Image Credits: Julia Lemba

Image Credits: Julia Lemba Welcome back to The Interchange! If you want this in your inbox, sign up here. We’re back after a brief hiatus, with lots of fintech news, including Robinhood’s latest acquisition, Plaid’s newest product and a ChatGPT-powered AI tool that aims to help you save money on bills.

Mary Ann Azevedo, Christine Hall

Robinhood’s motives

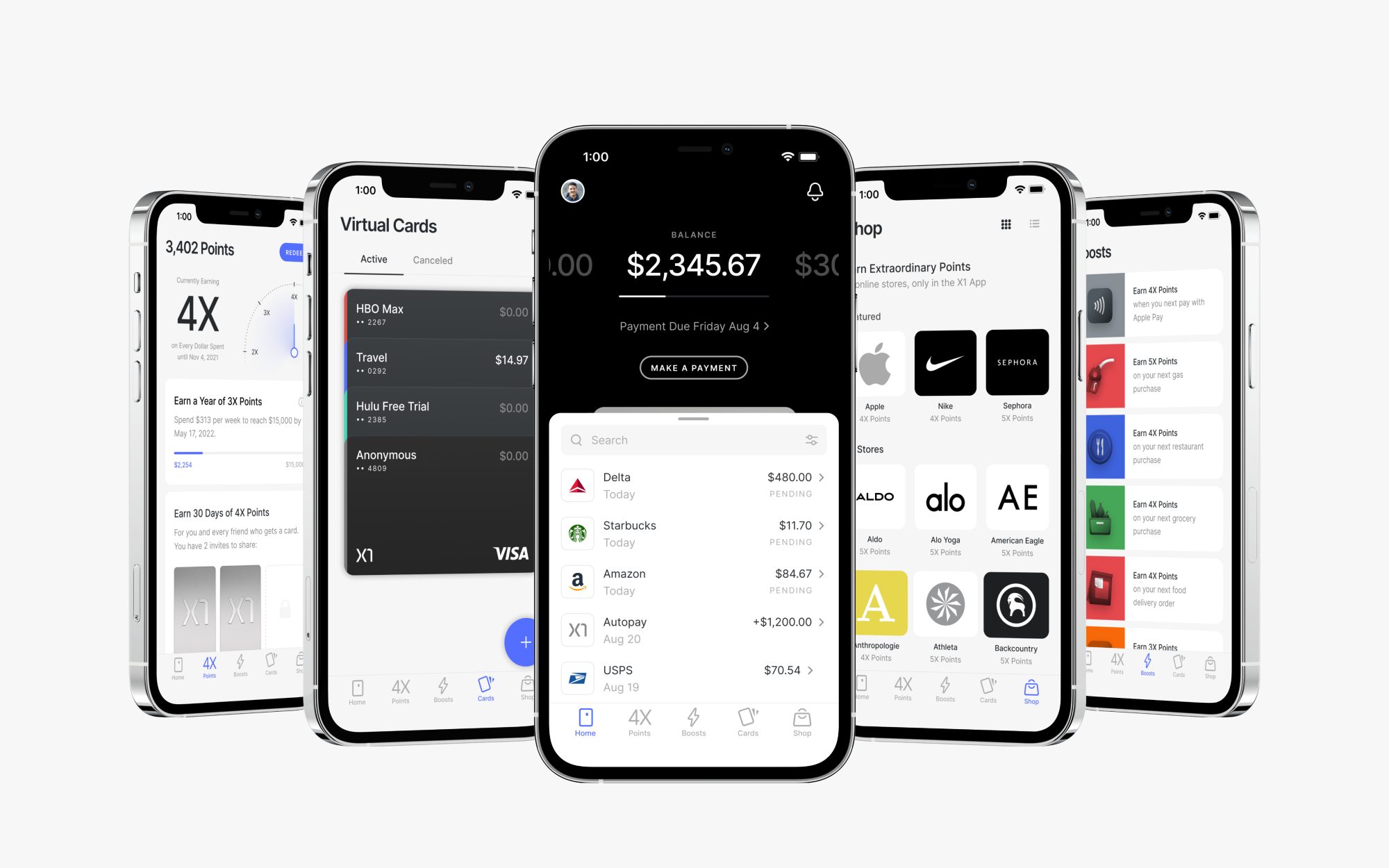

When Robinhood announced on June 22 that it was acquiring credit card startup X1 for $95 million, it caused all sorts of chatter in the fintech world.

Why would Robinhood want to buy a credit card startup? Did it get a good deal, considering that X1 has raised only $62 million over its lifetime? Did its investors get a good deal or just a return on their investment? Why X1 in particular over the many other credit card startups out there?

Let’s talk about that last point first.

When we talked to X1 in December at the time of its last fundraise, founder and CEO Deepak Rao told us the company was launching a new trading platform that would give its cardholders the ability to buy stocks by using earned reward points. He even singled out Robinhood as a company he was hoping to compete with, telling TechCrunch: “By using credit card points to buy stock instead of cash or their savings, we feel this is a safe way for many consumers to start investing. There is no real downside as their investing is technically free.”

Aha.

Could that be what drew Robinhood to X1??

On this week’s Equity podcast, we chatted about that possibility, with co-host Alex Wilhelm noting that one would have to earn a lot of rewards before being able to buy many stocks. He also pointed out that Robinhood perhaps had some money to burn, as well as the company declaring that it was looking for something new as a way of “broadening [its] product offerings” and “deepening” its relationship with existing customers.

If you’ve been following Robinhood’s performance over the past year, a desire to diversify its business is probably not a surprise. We noted that not only has Robinhood’s crypto trading slowed, but also the company has seen significant user attrition. So an X1 acquisition gets Robinhood into the credit card space and an additional revenue stream.

Still, one observer noted that while X1’s basic premise of offering credit based on income rather than credit score was innovative, since it first formed in 2020 it has not really since delivered anything — other than the new stock feature — that stands out in the market.

Fintech analyst Alex Johnson shared a similar sentiment, tweeting: “The brand alignment is strong. Both companies have a certain unearned machismo about them. Other than that though, I don’t get this for Robinhood. X1 doesn’t have a lot of customers (did it ever even fully launch?) and none of its features are revolutionary.”

It is true that X1 may not have had a lot of customers, especially in comparison to a giant like Robinhood, but the company claimed to be on a growth trajectory, with Rao telling us last December that the company saw $3 million a month in revenue last October, giving it an annual revenue rate of $36 million.

Not everyone is down on the deal, though. Better Tomorrow Ventures’ Sheel Mohnot tweeted that while X1 may not have a lot of customers, Robinhood does. He added: “[T]his seems like a good acquisition to me, cheaper to cross-sell than to sell to new customers.”

— Mary Ann and Christine

.png)

.jpeg)

0 Comments